Unlock the Secrets of the HSA! Trends, How to Qualify, & Usage

“Never spend your money before you have it.”

-Thomas Jefferson

Health savings and flexible spending accounts are the crossover between money and medicine. Since deductibles are rising, ordinary care is becoming an out of pocket expense. This is not a personal finance blog at all, but after this post you’ll be able to take advantage of benefits for your health and maybe even your pocketbook.

Today’s TLDR—if you’re spending money on healthcare, at least get some pretax benefits with that

More routine healthcare is out of pocket than ever before: average deductibles have risen 40-50%+ since 2013!

Go get an HSA if your medical insurance deductible is >$1600 (individuals) or $3200 (family)

Then actually use the HSA (make full contributions if possible, avoid holding cash unless you know you need to incur an expense)

Inquire about an FSA from your employer if that applies

Health Savings What-now?

The main concept here is that health savings accounts, or HSAs, and flexible spending accounts, or FSAs, have pretax money that you can spend on various healthcare items. Drugs? Yes. Office visits? Yes. The HSA bank and IRS websites detail what expenses are eligible. You could use HSA funds for a non-medical expense but you won’t get any reimbursement or credit. It also doesn’t hurt to check to your original HSA or FSA plan document to get more specifics. Most people get a debit card for the account. It’s a little machete to defend yourself against an ever-growing thicket of healthcare expenses. Better to have one than not.

Most of time, you sign up for HSAs via your employer

The HSA is easier to understand so we’ll start there—with this account, you or your employer make tax-deductible contributions which you can use for things like medical visits and prescriptions. A couple neat facts about HSAs is that 1) your unspent money generally rolls over every year and 2) that you can invest those funds like you would an IRA or 401(k). This all sounds wonderful, but there are some limits. You can only qualify for an HSA if you have something called a “high deductible health plan (HDHP).” Meaning: your insurance requires you to spend a certain amount out of pocket before coverage starts. The IRS defines these plans as having a deductible of $1600+ for individuals and $3200+ for families. So if you’re spending money for medical care and medications, you get some tax relief on top. The share of employees enrolling in HSAs (24% in 2023) more than doubled since 2013 (11%).

The rising tide lifting too many boats

As you know, inflation is a persistent beast, especially over the past four-plus years. Health plan deductibles are rising too. It sounds like a bit of injustice—you’re paying more and more for medical coverage, but the initial out of pocket requirements grow as well. There’s a silver lining: more Americans may then qualify for HSAs. Per the Consumer Financial Protection Bureau’s 5/2024 report, there were 36M HSAs reported in 2023 reflecting $116B of assets.

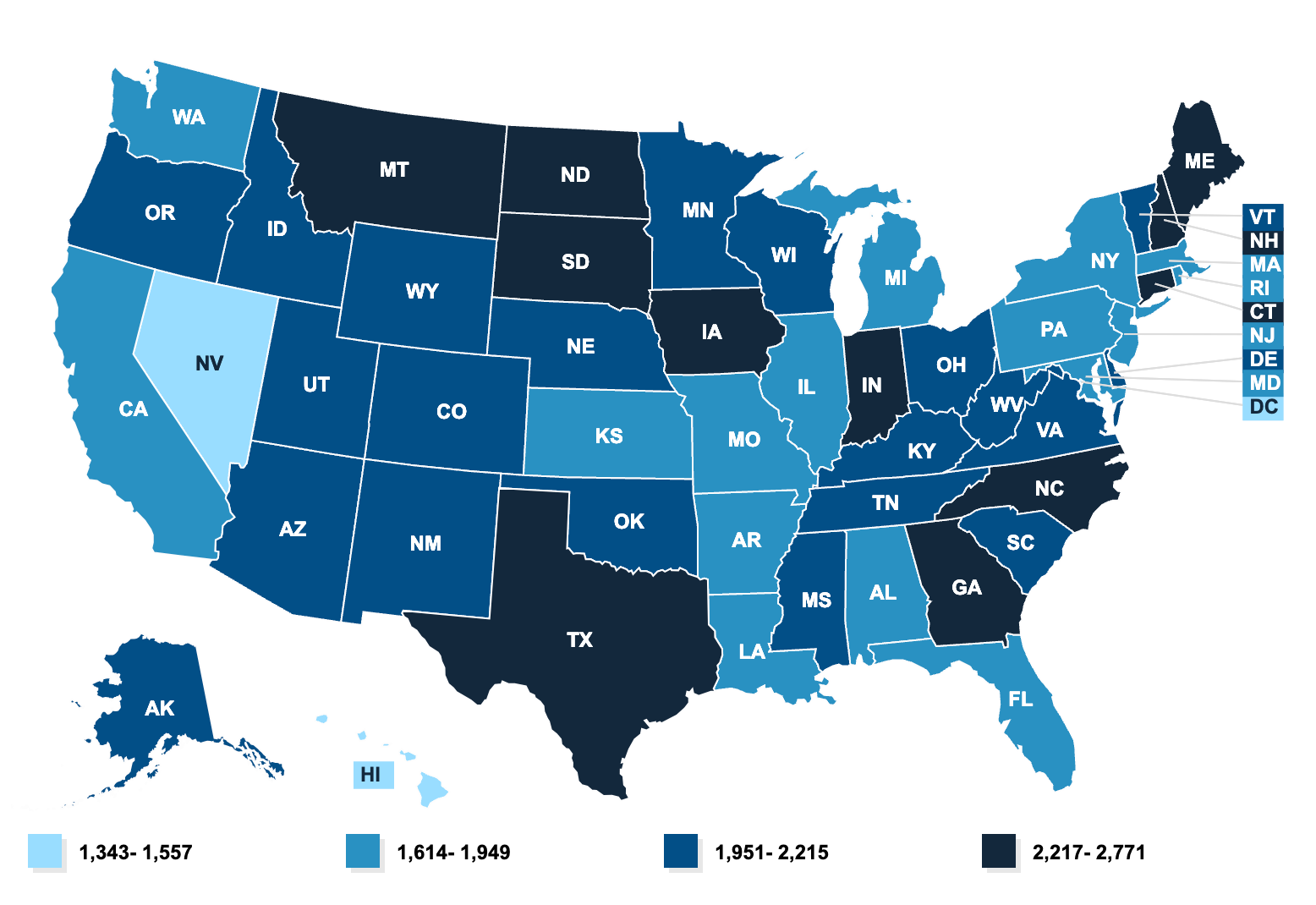

Even if people can acquire an HSA, that doesn’t mean it’s handled properly. Many of those accounts are underutilized. The Employee Benefit Research Institute (EBRI) found that individuals only contribute ~78% of the annual max allowable limit (although this has improved over recent years). Just ~13% of account holders acquired investments other than cash. This long-term study (from 2011 to 2022) also found a wide deductible variation between states. Consult the map below for your state.

Out of pocket requirements are climbing everywhere. Hence why it’s in your best interest to be not only prepared but also more choosy with your healthcare.

Signed up for an HSA? Nice. But…

…you still have to be vigilant. Depending on the financial institution you pick—HealthEquity, Optum, and Fidelity are the top three by assets—there can be account fees. Some might feel like this is a tax on breathing. Fees are, and always have been, the enemy of returns. The bottom line is to be mindful of what you’re paying. Keep your statements. If switching employers (or an HSA provider with the same employer), watch for unexpected account charges or transfer fees.

Also be mindful of interest rates the HSA providers offer for cash or money market positions. Even with the current macro environment of higher rates, the yield may vary significantly between <1% to <5%. Make sure you’re at least doing better than inflation—the US had 2.9% inflation in the 12 months ending in July 2024. Otherwise you’re losing money in real terms. No one likes to walk forwards but move backwards. Unless you can do a moonwalk.

The FSA—The HSA’s weird cousin

Unlike their counterpart, FSAs exclusively come from your employer through a pretax payroll deduction. Some workplaces have more or less restrictions on eligible uses beyond whatever the IRS suggests. You don’t need a high deductible health plan to get an FSA. The confusing part happens when you realize there is more than one type of FSA. This is just classic healthcare making life complicated, but I’ll break down the major types. Although your average FSA can fund medical costs just like the HSA, some companies offer a limited-use version with money only eligible for dental and vision care. You might also see a dependent care plan, or DCFSA, meant for child care, elder care, or some preschool services.

Unlike the HSA though, you can’t rollover all your unspent funds. The IRS has a 20% contribution rollover limit for FSAs every year but your employer makes the final decision on what’s okay. Because of the Covid-19 pandemic and the 2021 American Rescue Plan Act, there are exceptions in place, so you can ask your tax preparer about that if needed. If you have the luxury of being able to choose between an HSA and FSA, you should think about your medical habits and tendencies so you can make the most of either plan.

From money to medicine

Regardless of how you choose to spend all that hard-earned pretax money, any healthcare expense should be made at a clinic that treats you well. Contact us on Substack or @caretocash on x.com for personalized guidance on navigating your healthcare journey.